Once upon a time, over 20 years ago, a tax officer informed Company J, which manufactures electronic components for export to its parent company in Japan, that “companies in the electronic components manufacturing industry have an average operating profit margin of 15%.” Consequently, the officer reassessed Company J’s profit margin from 3% to 15% and issued a notice of additional tax payment, including penalties and surcharges. If you were the managing director of Company J, how would you explain this?

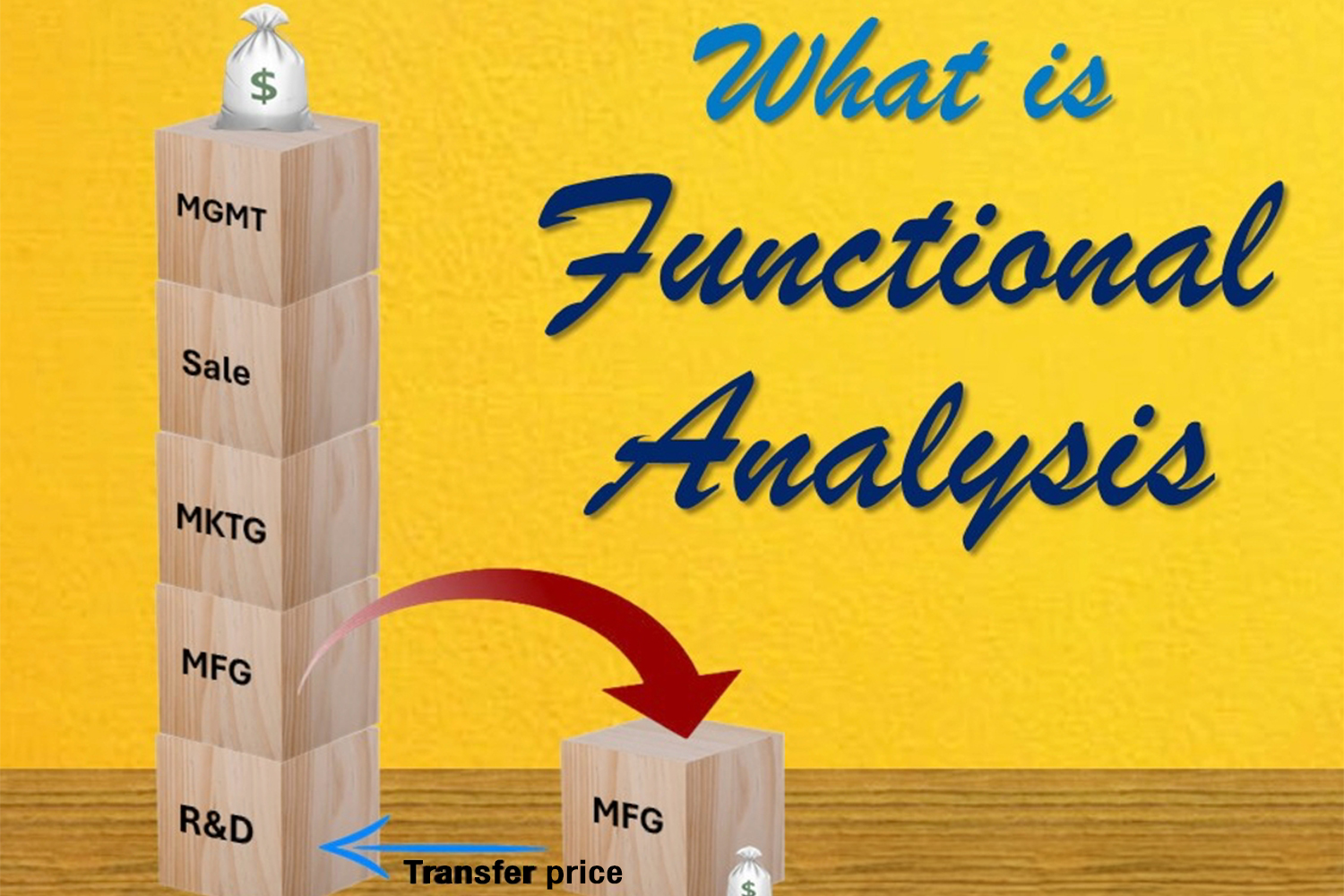

The answer lies in the company’s Functional Profile—the nature of the functions a company performs and the activities it undertakes, considering the risks it assumes and the assets it uses [Ref.: OECD Guidelines, 2022, Chapter III. Comparability Analysis, paragraph 1.51]. If we compare a company to a set of building blocks (as shown in the illustration), each block represents a function the company performs. In the example, there are five blocks, i.e., R&D, production, marketing, sales, and administration. In modern jargon, this company is a “fully-fledged.” Historically, Company J was just a factory of the parent company, which was later relocated its production base to Thailand—possibly to reduce costs due to proximity to raw materials or markets, or perhaps BOI’s tax incentives. Company J thus only performs and assumes risks related to manufacturing components for the parent company, similar to an OEM (Original Equipment Manufacturer) that produces goods for various brands (represented by the single block on the right in the illustration). This necessitates the determination of “transfer prices” when selling products back to the parent company. Since Company J only performs and assumes risks related to production, its profit margin—linked to its function—is significantly lower than that of independent companies with full functions [Ref.: OECD Guidelines, 2022, paragraph 1.56].

Today, this explanation carries more weight as it aligns with the practices outlined in the Director-General’s Notification on Income Tax No. 400, Clause 4, which requires a comparability analysis before analyzing profit margins for tax assessment. The functions of the contracting parties are one of the five key factors that must be considered.

However, Thai law does not provide detailed guidance on Functional Analysis. Therefore, we rely on the OECD Guidelines [paragraphs 1.60–1.126], which focus on analyzing commercial and financial risks. The process can be summarized as follows:

(a) Identify significant risks, typically by following the steps in the value chain.

(b) Analyze (along with contractual terms) which company assumes and manages each risk. The risk bearer and risk manager may be separate entities.

(c) Determine whether the company’s operations align with the contractual risk assumptions.

(d) Assess whether the company has the capability and financial capacity to manage those risks.

Caution: Under step (c), verifying the consistency between contractual risk assumptions and actual operations is crucial. For example, if Company J explains to the tax officer that its lower profit margin compared to independent companies in the same industry is due to its limited functions and risks—only manufacturing for the parent company—this must not be merely stated on paper. If the officer checks the organizational chart, there should be no departments related to R&D, marketing, or sales. If such departments exist, they should not have significant responsibilities or staffing.

[Contact Person: Mr. Phongnarin Ratarangsikul | Partner]