The Cabinet on 15 June 2026 endorsed key measures proposed by the Ministry of Finance to accelerate the Revenue Department’s digitalization of the tax system by extending the measures which already ended in 2025, to be effective from 1 January 2026 to 31 December 2027.

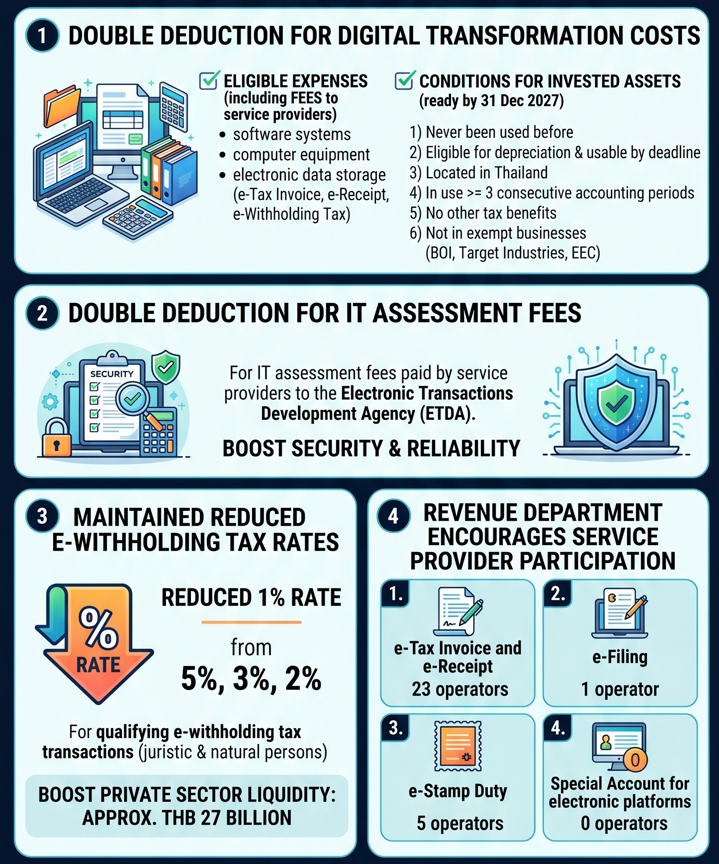

First, the measure offers double deduction of expenses related to digital transformation costs. Eligible expenses include investments in software systems, computer equipment, electronic data storage systems for e-Tax Invoice, e-Receipt, and e-Withholding Tax.

Assets invested by taxpayers must meet the following conditions:

1) Never been used before;

2) Be eligible for depreciation and acquired and in usable condition within 31 December 2027;

3) Located within Thailand;

4) Be in use for a period of not less than 3 consecutive accounting periods, starting from the first accounting period in which it was acquired and became ready for use;

5) Not an asset eligible for any other tax benefits, whether in whole or in part; and

6) Not used in businesses that are exempt from taxes under the Investment Promotion Act, the Act on Enhancing the Competitiveness of Target Industries, or the Eastern Economic Corridor Act, whether in whole or in part

This double deduction of expenses also applies to the case of fees paid to electronic tax service providers.

Second, to boost the security and reliability of government digital systems, the measure offers a new double deduction tax incentive for IT assessment fees paid by service providers to the Electronic Transactions Development Agency (ETDA).

Third, the measure maintains a reduced 1% withholding tax rates from 5%, 3% and 2% for qualifying e-withholding tax transactions derived from payments of disposable income to juristic persons and natural persons. This measure is expected to boost private sector liquidity by approximately THB 27 billion.

Fourth, the Revenue Department also encouraged enterprises to take part in providing services in preparation and submission of electronic data in four areas as follows:

1) e-Tax Invoice and e-Receipt (currently 23 operators);

2) e-Filing (currently 1 operator);

3) e-Stamp Duty (currently 5 operators); and

4) Special Account for electronic platforms (currently no operator).

Author's Notes:

The government’s ongoing shift toward digitalization is expected to improve operational efficiency for both taxpayers and the Revenue Department. Promoting double deduction for fees paid to service providers would mitigate cost burden of smaller taxpayers who desire to join electronic tax systems. In longer run, this paperless system would minimize their operational costs. This window of opportunity would last until 31 December 2027. From the Revenue Department’s perspective, these measures would also facilitate the inclusion of taxpayers of all sizes into the tax systems.

In all, electronic tax systems would enhance transparency in tax compliance while enabling the Revenue Department to more effectively identify and address non-complaint behavior of the taxpayers. Accordingly, the taxpayers should ensure the accuracy of their tax compliance at all time.

[Contact Person: Ms. Susama Thaveesin, Director]